Why AI Efficiency Outruns Hardware Shortages

Time Bought, Advantage Lost? The Limits of Semiconductor Sanctions

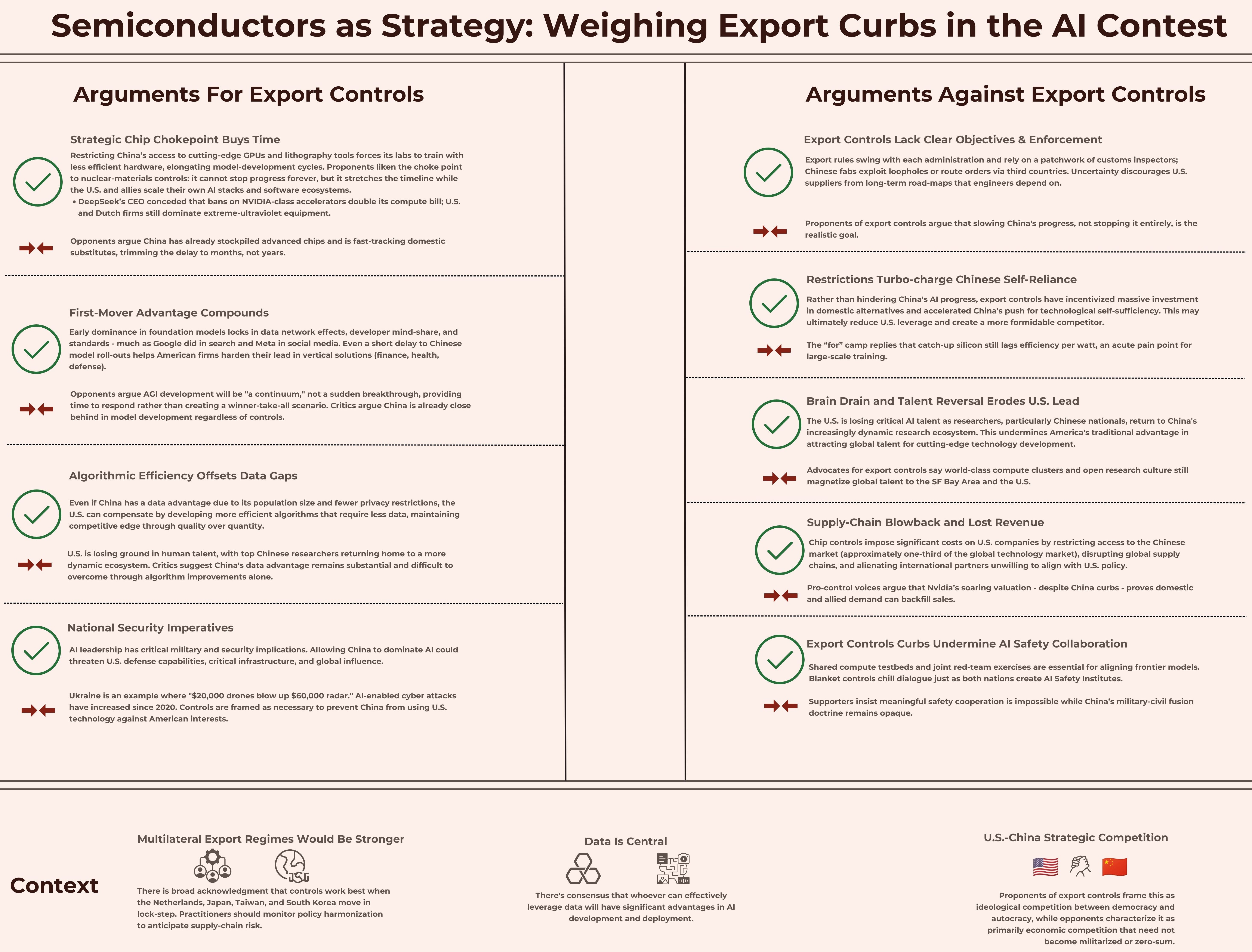

The technological and economic competition between the United States and China has increasingly centered on AI capabilities, with semiconductor access becoming the critical battleground. Since 2022, these export controls have evolved from targeted restrictions to a complex regulatory regime with far-reaching implications.

I have tracked Washington’s semiconductor export controls since they were first rolled out, and at the time laid out their strategic purpose: lengthen China’s AI development timetable by choking off top-tier GPUs. The basic logic still holds - swapping in domestic accelerators is harder than replacing a line of code - but the execution has drifted. Rules have multiplied, carve-outs have proliferated, and American suppliers now face almost as much uncertainty as the Chinese labs the policy targets. Washington’s rulebook is now in flux: one set of controls was withdrawn before it even took effect, and officials say a replacement will emerge only after further consultation.

The aborted Biden administration regulation would have imposed national caps limiting American cloud providers to housing no more than 7% of their global AI capacity in countries like Malaysia - a restriction that Oracle was already set to exceed. Beyond the corporate confusion, the diplomatic damage was immediate: European officials publicly accused Washington of creating a two-tier system that would push over 100 nations toward Chinese suppliers. The Trump administration now faces the delicate task of crafting rules that satisfy domestic security hawks, reassure allies, and avoid creating incentives for third-country shipment schemes that are already complicating enforcement.

My recent deep dive into Huawei’s Ascend ecosystem shows how that uncertainty has galvanized China’s hardware push. Ascend clusters still lag NVIDIA on power efficiency, yet each generation trims the deficit, and the supporting software stack is maturing quickly. Having chaired AI conferences in Beijing, I have watched domestic rivals push one another at a pace that rivals innovation in Silicon Valley. This intense domestic competition means a handful of Chinese players are likely to keep closing whatever hardware and modeling gap remains.

China's semiconductor resilience extends beyond chip design to manufacturing infrastructure. In 2024, Chinese entities imported $30.9 billion in chipmaking equipment - with Japan and the Netherlands supplying two-thirds of that total. This represents a deliberate stockpiling strategy ahead of anticipated export restrictions. More significantly, domestic equipment makers like Naura Technology are capturing market share from American suppliers in critical areas like etching and deposition tools. The shift suggests that even if chip controls succeed in the short term, China is methodically building the industrial base to circumvent them entirely within five years.

In May Tencent’s president told investors the firm has “ample high-end chips” for several more training cycles, thanks to software tricks that wring more value from smaller clusters. Far from slowing Beijing’s giants, the controls have nudged them to prioritize efficiency - and to scour the market for compliant accelerators and ASICs.

These efficiency improvements are not merely theoretical. Chinese firms report achieving comparable training results with clusters one-fifth the size previously thought necessary, effectively multiplying their GPU capacity through software optimization alone. The shift away from brute-force scaling represents a fundamental rethinking of AI development methodology - one that could render hardware restrictions less effective than policymakers anticipated.

The real battleground has shifted from raw capability to deployment velocity. While Silicon Valley debates the path to artificial general intelligence, Chinese firms are embedding AI into manufacturing lines, logistics networks, and consumer applications at unprecedented scale. DeepSeek's models, optimized for inference efficiency rather than benchmark performance, are finding eager customers from Jakarta to Cairo. The irony is striking: export controls designed to maintain American AI leadership may be accelerating the global adoption of Chinese alternatives, particularly in markets where cost-effectiveness and local deployment matter more than cutting-edge performance.

China’s push for self-reliance is not confined to chips. From electric-vehicle batteries to commercial satellites, Beijing is ploughing hundreds of billions of dollars into R&D and telling firms to out-compete one another. The result is impressive speed but mounting debt and occasional graft - signs of a state-led investment binge that may yet prove unsustainable.

This complex dynamic means that export controls, as a policy tool, are being asked to achieve multiple, sometimes conflicting, goals: maintaining a national security advantage, supporting domestic chip industries, and even fostering AI safety. However, a focus on hardware alone is too narrow. Progress in algorithmic efficiency is one such factor, but I believe the global flow of talent is even more decisive. For decades, America’s greatest asymmetric advantage has been its ability to attract the world’s top scientific minds. They form the bedrock of graduate programs in computer science and engineering and go on to found a majority of the country's leading AI firms. To put this vital pipeline at risk with blunt immigration restrictions seems profoundly self-defeating; it is a strategy that seems purpose-built to help America’s rivals close the gap.

America’s greatest asymmetric advantage has been its ability to attract the world’s top scientific minds … To put this vital pipeline at risk with blunt immigration restrictions seems profoundly self-defeating.

If the next revision of export rules is not paired with a broader industrial and research strategy, the United States may find it has won a narrow skirmish over chips while ceding ground in the wider struggle for practical AI deployment. Washington therefore needs twin-track discipline: surgical restrictions on truly militarily sensitive hardware, and a coherent industrial strategy that accelerates domestic fabs, talent visas, and energy-hungry data-center build-outs at home.

{kind=link}

Ben Lorica edits the Gradient Flow newsletter. He helps organize the AI Conference, the AI Agent Conference, the NLP Summit, Ray Summit, and the Data+AI Summit. He is the host of the Data Exchange podcast. You can follow him on Linkedin, Mastodon, Reddit, Bluesky, YouTube, or TikTok. This newsletter is produced by Gradient Flow.